The recent Fed rate cut marks a pivotal shift in the U.S. economic landscape, signaling the first significant reduction in four years. As the Federal Reserve decreases the cost of borrowing, this move is expected to greatly influence mortgage rates, making it easier for homebuyers to achieve housing affordability. Economists predict that this easing of monetary policy will not only aid consumers with credit card debts and loans but also bolster economic growth. In the face of inflationary pressures, the impact of rate cuts becomes crucial in shaping market dynamics and consumer confidence. With more rate reductions possibly on the horizon, the effects on various sectors of the economy, including housing and investments, will be closely watched in the coming months.

A recent decision by the central bank to lower key borrowing costs represents a significant evolution in monetary policy, reflecting a strategic response to recent economic conditions. This reduction, known as a rate cut, aims to stimulate spending and investment, ultimately supporting broader economic stability. As lower interest rates encourage homebuyers and ease debt burdens, they play a crucial role in enhancing housing affordability issues and fueling economic growth. The effects of these changes ripple across sectors, influencing everything from consumer financing to investment strategies. As financial markets and households adjust to this new policy environment, understanding its implications will be essential for navigating the evolving economic landscape.

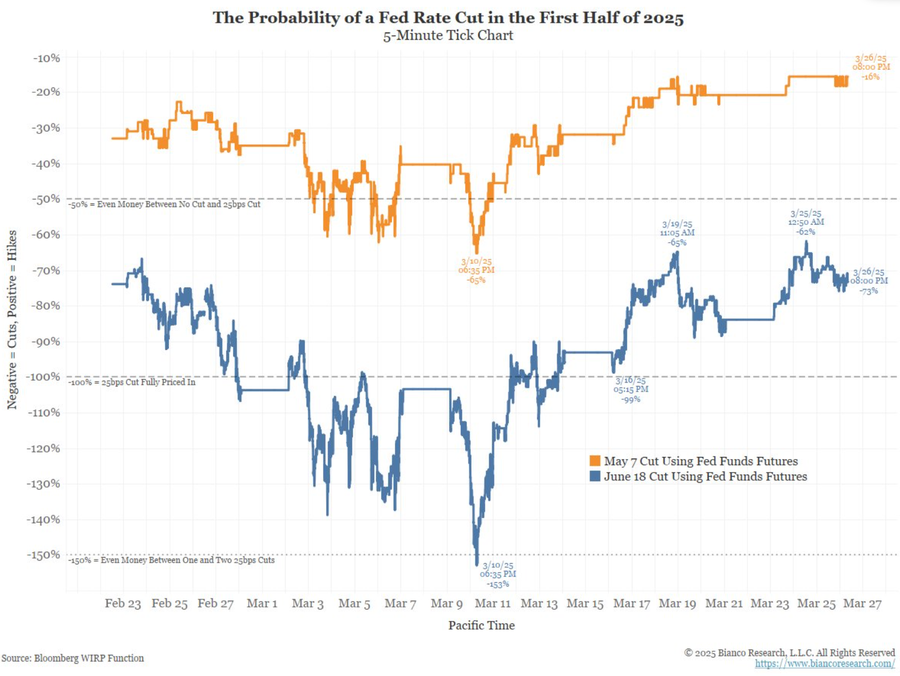

Understanding the Impact of the Fed Rate Cut

The recent Fed rate cut is significant as it marks the first major reduction in four years, signaling a shift in monetary policy aimed at stimulating borrowing and spending. This decision is expected to ease the financial burden on consumers, particularly for those dealing with credit card debt, car loans, and mortgages. As the Federal Reserve lowers the cost of borrowing, it is likely that consumers will begin to see lower interest rates, providing them with some relief and enabling them to allocate their finances toward other areas of the economy.

Moreover, this proactive move by the Federal Reserve sets a positive tone for economic growth by encouraging consumers to spend more, which could help sustain the ongoing recovery. The Fed has indicated that if economic conditions warrant it, they may initiate further cuts, thereby fostering a climate of confidence and stability in the market. Consequently, the long-term impacts of these rate cuts could lead to improved economic health overall, boosting consumer confidence, which is pivotal for future spending and investment.

Mortgage Rates and Housing Affordability Post Fed Rate Cut

With the Fed’s decision to lower interest rates, mortgage rates are expected to gradually decline, providing much-needed help to homebuyers who have faced increasing challenges in housing affordability. As the costs of borrowing drop, potential homeowners may find it easier to secure loans, ultimately enhancing their ability to purchase homes and contributing positively to the housing market. This dynamic is critical, as many individuals have been priced out of the market amid rising rates in previous months.

This anticipated decline in mortgage rates is not just a temporary fix but part of a broader strategy to alleviate the housing affordability crisis, especially for first-time buyers. The Fed’s current stance on maintaining an easing policy is crucial, as it encompasses the necessity for sustained economic growth while addressing challenges within the housing sector. However, while lower mortgage rates can make homes more accessible, systemic issues regarding inventory and housing supply must also be addressed to ensure lasting improvements in affordability.

Consumer Debt and the Outlook for Lower Interest Rates

Following the Fed’s rate cut, consumers are likely to benefit from a slight reduction in the overall interest rates they pay on various debts. As the economy adjusts, interest rates for credit cards, personal loans, and car loans could begin to drop, providing relief to consumers who have been struggling with high payments. However, the timeline for experiencing these benefits remains uncertain as many lenders take time to adjust their rates to mirror the changes in the Federal Reserve’s policies.

Ultimately, while there may be some delays in the actual realization of lower rates, the insight from economists suggests that consumers should anticipate gradual relief over the coming months. It is essential for borrowers to stay informed about the shifting interest rates and account for the fact that not all interest rates will decline uniformly, as factors such as repayment risk and lender policies also come into play.

The Federal Reserve’s Strategy for Economic Growth

The Federal Reserve’s recent decision reflects a broader strategy to support economic growth while balancing inflation. By cutting rates, the Fed aims to spur spending and investment, which can lead to increased job creation and an uplift in economic activity. This approach is particularly beneficial in a time when inflationary pressures are being monitored closely and a delicate balance must be maintained to avoid extremes of economic downturn.

Furthermore, if economic indicators show signs of deterioration, such as rising unemployment rates, the Fed has signaled readiness to implement additional cuts. This flexibility in monetary policy showcases the Fed’s commitment to reacting promptly to economic shifts, ensuring that the recovery remains on track. As a result, businesses and consumers alike can navigate these fluctuations with more confidence, knowing that the central bank is proactively managing the economy.

Key Considerations for Investors After the Fed Rate Cut

Investors should take a nuanced approach following the Fed’s rate cut, understanding the potential repercussions for various sectors of the economy. Lower interest rates typically have a positive impact on stock prices, as companies may benefit from cheaper borrowing costs, leading to expansion and improved profitability. However, the timing and extent of these benefits will largely depend on investor sentiment and broader market conditions in the wake of the rate changes.

Moreover, investors should also consider the interconnectedness of different asset classes in this environment. For instance, while equities may rise, real estate investments and REITs could see a more immediate positive impact from lower mortgage rates, enhancing their attractiveness. Therefore, strategic allocations may need to be reassessed to capitalize on the changing landscape effectively.

The Future of Economic Recovery Amidst Rate Cuts

The anticipated effects of the Fed’s rate cuts extend beyond immediate borrowing costs. They are expected to play a pivotal role in shaping the economic recovery trajectory over the next few months. As consumer confidence grows, spending may increase, propelling economic recovery further and allowing businesses to thrive amid favorable borrowing conditions. With the Fed’s indication of potential additional cuts, there’s a level of optimism surrounding sustainable economic growth.

However, alongside these positive expectations, there are underlying challenges that need to be addressed, including labor market fluctuations and inflation control. As the Fed navigates these complexities, their policies will be pivotal in determining whether the current recovery can transform into lasting momentum and increased resilience in the economy.

Housing Market Dynamics Following Fed Rate Cuts

The housing market is expected to experience a shift in dynamics following the Fed’s latest rate cuts. With lower borrowing costs, prospective homebuyers may find themselves in a better position to enter the market, potentially reversing some of the affordability issues that have plagued many regions. As mortgage rates decrease, the prospect of homeownership becomes more viable for those who might have been reluctant due to previous high-interest scenarios.

However, the improvement in affordability will not solely hinge on lower interest rates. Broader factors such as housing supply, regional market conditions, and the ongoing impact of economic growth will also play critical roles. It is essential for policymakers to remain attentive to these elements to foster a truly balanced housing market capable of sustaining growth over the long term.

Exploring Economic Indicators Influencing Fed Decisions

The Federal Reserve relies on a variety of economic indicators when making decisions about interest rates, including unemployment rates, inflation data, and consumer spending patterns. Understanding how these indicators interact helps provide clarity on why a Fed rate cut might be necessary at any given time. As the Fed monitors these indicators, they remain focused on maintaining a stable economic environment that encourages growth while keeping inflation in check.

The importance of accurate data interpretation cannot be overstated. A sudden increase in inflation, for instance, could prompt the Fed to reconsider their current course despite recent rate cuts. Therefore, investors and consumers alike should keep a close eye on these economic indicators, as they hold significant implications for future Fed actions and overall market health.

Consumer Expectations in a Rate Cut Environment

In the wake of the Fed’s rate cut, consumer expectations are poised for change, as individuals anticipate improved financial conditions ahead. Lower interest rates can create a sense of optimism among consumers, influencing their purchasing behavior and willingness to take on loans for major purchases such as homes, cars, and education. Consequently, this shift in expectations can have ripple effects across the economy, spurring increased activity in retail and services.

It is important, however, for consumers to remain cautious. While the Fed’s actions can create favorable borrowing conditions, individuals should also be mindful of broader economic factors that may affect their financial decisions. Staying informed regarding economic trends and rate adjustments will empower consumers to navigate this uncertain environment effectively, making smart decisions based on both current conditions and future projections.

Frequently Asked Questions

What is a Fed rate cut and how does it impact consumers?

A Fed rate cut is when the Federal Reserve lowers its benchmark interest rate, making borrowing cheaper. This can decrease interest rates on loans and credit products, ultimately benefiting consumers by making mortgages, credit cards, and auto loans more affordable. As a result, consumers may see lower monthly payments and improved cash flow.

How do Fed rate cuts affect mortgage rates and housing affordability?

Fed rate cuts typically lead to a decline in mortgage rates, making housing more affordable for potential buyers. As the Federal Reserve eases its monetary policy, borrowers may benefit from lower mortgage rates, which can ease the housing affordability crisis by allowing more consumers to enter the housing market.

What is the expected impact of Fed rate cuts on economic growth?

The impact of Fed rate cuts on economic growth is generally positive, as lower borrowing costs can stimulate spending and investment. This can lead to job creation and higher consumer confidence, contributing to overall economic expansion. However, the effects may take several months to materialize fully.

Will further Fed rate cuts affect credit card interest rates?

Yes, further Fed rate cuts may eventually lead to lower credit card interest rates, as these rates are often influenced by the Fed’s actions. However, the timing and extent of these adjustments can vary based on market conditions and consumer repayment risks.

How frequently does the Fed cut rates, and what signals do they send to the market?

The Fed usually cuts rates in increments, commonly by 0.25% or 0.50%. They provide forecasts during meetings that signal potential future rate changes. For example, the recent Fed rate cut has indicated the likelihood of additional cuts, influencing market expectations and lending behavior.

What should consumers do to prepare for a changing interest rate environment after a Fed rate cut?

Consumers should review their finances, considering refinancing options for mortgages or consolidating high-interest debt as rates decrease. Staying informed about future Fed actions can help individuals make strategic decisions regarding lending products to maximize benefits.

What are the long-term expectations for interest rates following a Fed rate cut?

Following a Fed rate cut, interest rates might stay lower for an extended time as the economy adjusts. However, external factors such as inflation and economic performance could alter this trajectory, making it essential to stay updated on economic indicators.

| Key Point | Details |

|---|---|

| Fed Rate Cut | The Federal Reserve cut the key interest rate by 0.5% for the first time in four years. |

| Economic Impact | The cut is expected to benefit consumers with credit card debt and mortgages, as borrowing costs will decrease. |

| Future Projections | Analysts predict the possibility of two additional rate cuts before year-end, depending on upcoming economic data. |

| Market Reactions | The market may adjust rates further in anticipation of Fed actions, especially if economic indicators like unemployment worsen. |

| Home Affordability | Mortgage rates are likely to decline further, improving affordability, but remain relatively high. |

| Consumer Expectations | While some relief in interest rates is anticipated, significant changes may take time and rates may not drop drastically soon. |

Summary

The Fed rate cut marks a crucial shift in monetary policy aimed at supporting economic stability. While consumers may benefit from lower borrowing costs, the extent and timing of these changes remain to be seen. The Fed’s decision to lower rates is designed to bolster job growth and alleviate financial pressures faced by borrowers. Understanding how these adjustments play out in the housing market and overall economy will be essential in the coming months.