The 2017 Tax Cuts and Jobs Act (TCJA) marked a pivotal moment in the U.S. tax policy landscape, fundamentally reshaping the approach to corporate taxation. This sweeping reform slashed corporate tax rates from 35% to 21%, aiming to stimulate investments and spur economic growth across the nation. However, as the tax policy impact unfolds, the debate continues regarding its effectiveness in boosting wages and productivity while simultaneously leading to a tax revenue decline for the federal government. One of the key features of the TCJA was the expansion of the Child Tax Credit, which sought to alleviate financial burdens for families. As Congress approaches another tax battle in 2025, understanding the economic implications of the TCJA remains crucial for voters and policymakers alike.

Referred to as the TCJA, the Tax Cuts and Jobs Act of 2017 introduced significant changes to the fiscal framework in the United States, particularly in how corporate earnings are taxed. This legislation aimed to lower the burden on businesses and stimulate economic growth, but it ignited a contentious dialogue regarding its long-term sustainability and effects on tax revenue. The adjustments, including revisions to the Child Tax Credit, were intended to bolster financial relief for families while inciting increased investment from corporations. As discussions of new tax measures surface, evaluating the ramifications of this tax reform is vital in assessing future fiscal policies. The outcomes of the Act have led to varied perspectives on its role in reshaping the national economy and its broader impact on income distribution.

The Economic Impact of the 2017 Tax Cuts and Jobs Act

The 2017 Tax Cuts and Jobs Act (TCJA) significantly altered the landscape of corporate taxation in the United States by reducing the corporate tax rate from 35% to 21%. This landmark legislation was intended to stimulate economic growth, drive business investments, and ultimately create jobs. However, the economic implications of the TCJA are a matter of considerable debate among economists and policymakers. Proponents argue that lower corporate tax rates encourage businesses to invest in capital, which would lead to higher wages and increased hiring, thus benefiting the economy at large. Yet, studies, including recent analyses conducted by Gabriel Chodorow-Reich and others, suggest that the actual rise in wages and investments was modest, raising questions about the efficacy of the tax cuts as a growth strategy.

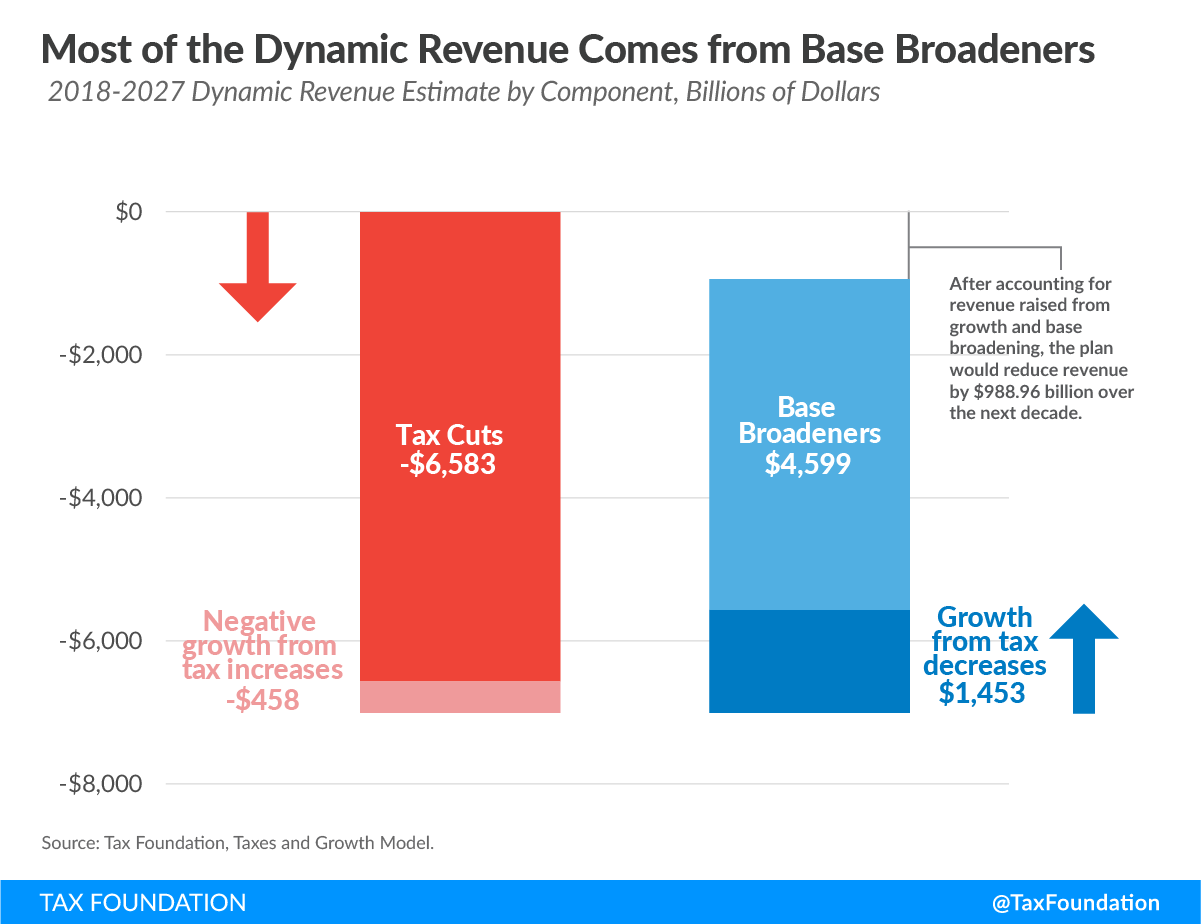

In examining the consequences of the TCJA, it is essential to consider not only the reduction in tax rates but also how it affected tax revenue. Contrary to expectations of a growth-driven tax revenue increase, the initial impact resulted in a pronounced decline in corporate tax collection, causing a budget shortfall that prompted concerns among fiscal policymakers. This decline in revenue underscores the fact that while corporate tax cuts may incentivize immediate investments, they may not alone sustain long-term economic health without careful legislative balancing.

Child Tax Credit: A Key Provision Under Pressure

One of the most significant provisions set forth in the TCJA was the expansion of the Child Tax Credit (CTC), aimed at providing financial relief to low- and middle-income families. This enhancement of the CTC was a critical selling point for the law, as it helped to alleviate child poverty and give families a much-needed financial boost. However, the temporary nature of many benefits under the TCJA, including the expanded CTC, creates uncertainty for families who depend on this financial support. With these provisions set to expire at the end of 2025, the ongoing political battle surrounding tax legislation becomes increasingly relevant for families across the nation.

The debate surrounding the renewal of the CTC is as contentious as the discussions regarding corporate tax rates. While Republicans may argue against an expansion due to concerns over tax revenue decline, many Democrats advocate for extending and even enhancing the Child Tax Credit to support working families. Recent analyses indicate that failing to renew these credits could lead to a significant rise in child poverty, further emphasizing the social implications of tax policy. Lawmakers must grapple with the trade-offs between sustaining tax revenue through corporate rate cuts and providing essential economic support to families through credits like the CTC.

Corporate Tax Rates: Should They Be Raised or Lowered?

The ongoing debate over whether to raise or lower corporate tax rates has gained significant traction as upcoming elections approach. Advocates for raising rates, including figures like Kamala Harris, suggest that a higher corporate tax could generate much-needed revenue to fund critical public initiatives. Meanwhile, opponents argue that further cuts to corporate tax rates will encourage economic growth, thus benefiting all sectors of society. This discussion reflects a broader questioning of tax policy impact and how such changes influence business behaviors and investment decisions.

Gabriel Chodorow-Reich’s recent study sheds light on this contentious issue by providing empirical evidence regarding the relationship between corporate tax rates and business investment. His findings suggest that while firms respond to changes in statutory rates, other mechanisms, like expensing provisions, may drive investment more effectively. This evidence complicates the narrative that simply lowering corporate taxes will inherently boost economic growth and invites a deeper exploration of how tax policies can be optimized to benefit both businesses and the broader economy.

The Future of American Tax Policy: Looking Ahead to 2025

As we approach 2025, the expiration of key provisions from the 2017 Tax Cuts and Jobs Act looms large on the horizon. Lawmakers will be faced with critical decisions regarding the direction of American tax policy and its implications for various demographics and business sectors. With significant cuts aimed at households and the Child Tax Credit set to expire, many voters are anxious about the potential impact on their financial security. The interplay of corporate and individual tax considerations will be paramount as discussions evolve into practical legislative action.

Moreover, the upcoming confrontation over the TCJA will not merely focus on the statutory rates alone but will also spotlight the overall structure of the tax code in response to a rapidly changing global economy. As economists like Chodorow-Reich advocate for a reconsideration of tax policy through comprehensive data analysis, the necessity for informed dialogue that transcends partisan divides becomes evident. A balanced tax reform could potentially lead to sustainable economic growth while addressing the pressing needs of American families.

Tax Revenue Trends: The Effects of TCJA

The implementation of the 2017 Tax Cuts and Jobs Act had a profound effect on federal tax revenue, resulting in an immediate 40% drop in corporate tax collections. Initially, this decline raised major concerns regarding federal budget deficits and the sustainability of public services funded by tax revenues. However, starting in 2020, there was a surprising rebound in corporate tax revenues, attributed mainly to a surge in business profits. Factors contributing to this rebound include changes in corporate profit booking practices and an unexpected economic recovery seen during the pandemic.

Understanding these trends requires nuance, as the dynamics of corporate taxation are influenced by numerous variables including international competition and the prevalence of tax injustices. As Chodorow-Reich suggests, further exploration into why corporate profits soared amid uncertainty is crucial. As we look ahead, careful consideration of these trends will guide policymakers in formulating tax strategies that not only stabilize revenue but effectively support economic growth.

The Debate Over Corporate Tax Policy: Partisan Divides

The discourse surrounding corporate tax policy has become increasingly polarized, with each party asserting differing perspectives on optimal tax structures. Congressional leaders have utilized proposals stemming from the 2017 TCJA to fuel their campaign narratives, with Democrats calling for increased corporate rates to amortize public expenditures while Republicans insist on maintaining or further reducing these rates to spur job growth. This ideological division poses challenges for achieving consensus on future tax reforms.

As exemplified by Gabriel Chodorow-Reich’s findings, the effectiveness of tax changes often depends on their design and the targeted incentives provided for businesses. The emerging question is how lawmakers can craft policies that restore fiscal balance while simultaneously fostering a favorable environment for business investment. Moving past mere partisan talking points will be essential for enabling constructive tax policy that addresses the diverse needs of the U.S. economy.

Exploring the Relationship Between Tax Policy and Investment

Investment behavior among businesses is significantly influenced by the prevailing corporate tax policy. A crucial point highlighted by recent studies is that significant incentives—such as expensing provisions—have been shown to mobilize capital investments effectively, sometimes outperforming standard rate cuts. This realization has challenged long-held beliefs regarding tax cuts as a primary motivator for businesses to inject capital into growth initiatives, urging lawmakers to consider how strategic tax incentives can be structured to bolster investment.

Chodorow-Reich suggests that supplementing tax revenue by adjusting statutory rates while reinstituting generous expensing policies could create a win-win scenario for businesses and taxpayers alike. The growing evidence indicates that a dual approach could not only enhance corporate behavior but also stabilize the broader economic landscape. This essential understanding encourages a more nuanced dialogue around tax reforms focusing on invigorating economic growth without sacrificing equity among varying stakeholders.

The Long-Term Effects of Tax Legislation on Wages

As discussions around the 2017 Tax Cuts and Jobs Act continue to evolve, one key area of evaluation remains the long-term effects of tax legislation on employee wages. Initial estimates suggesting potential wage increases of several thousand dollars were called into question by empirical studies, indicating much more modest gains. Chodorow-Reich’s analysis revealed that while some wage growth was observed, it fell short of the ambitious predictions that proponents of the TCJA put forth, demonstrating the complexities inherent in establishing direct causality between tax policy and wage changes.

These findings underscore the need for realistic expectations when assessing the effects of tax cuts on income levels. Lawmakers must take into account that while corporate tax policies can influence investments and growth, the corresponding impact on wages may not be as straightforward. As we move forward, fostering a productive dialogue centered on empirical evidence may lead to policies that more effectively enhance working conditions and compensation rates across the board.

Corporate Tax Reforms: Lessons Learned from TCJA

The 2017 Tax Cuts and Jobs Act provides numerous lessons for future tax reforms. As policymakers prepare for the upcoming legislative battle, reflecting on the successes and shortcomings of the TCJA will be critical. Insights gained from Gabriel Chodorow-Reich’s research emphasize the need for careful calibration of economic incentives that genuinely result in sustainable growth rather than short-term gains. Evaluations of previous tax reforms highlight the importance of balancing corporate interests with public welfare.

Additionally, understanding the nuances of how different tax provisions interact is essential for crafting effective policy. The lessons learned from the TCJA advocate for a proactive approach to tax reforms that targets real economic growth and aims to reduce social inequality. The future of American tax legislation should prioritize empirical analysis over partisan politics to develop solutions that work for both businesses and the American people.

Frequently Asked Questions

What are the key economic implications of the 2017 Tax Cuts and Jobs Act (TCJA)?

The 2017 Tax Cuts and Jobs Act (TCJA) significantly altered the economic landscape by reducing the corporate tax rate from 35% to 21%. This change aimed to stimulate business investment and economic growth. Research indicates that while corporate investments increased by about 11%, the overall impact on wages was more modest than expected, with annual raises averaging closer to $750 per full-time employee rather than the projected $4,000-$9,000.

How did the 2017 Tax Cuts and Jobs Act affect corporate tax rates in the U.S.?

The 2017 Tax Cuts and Jobs Act permanently reduced corporate tax rates from 35% to 21%, aligning U.S. rates more competitively with international standards. This reduction was projected to decrease federal corporate tax revenue by $100 billion to $150 billion annually for the next decade, prompting discussions on the long-term sustainability of tax policy post-TCJA.

What was the impact of the Child Tax Credit changes under the 2017 Tax Cuts and Jobs Act?

The 2017 Tax Cuts and Jobs Act expanded the Child Tax Credit, providing significant relief to low- and middle-income households. This provision is set to expire in 2025, raising concerns among voters regarding the future economic implications for families and the potential decline in tax revenue if these credits are not renewed.

Did the 2017 Tax Cuts and Jobs Act lead to a decline in tax revenue?

Yes, the 2017 Tax Cuts and Jobs Act resulted in a dramatic decline in corporate tax revenue, dropping by approximately 40% immediately after its implementation. However, corporate tax revenues began to rebound in 2020 as profits soared, leading to mixed evaluations of the law’s overall effectiveness in generating tax revenue.

What are the arguments regarding the tax policy impact of the 2017 Tax Cuts and Jobs Act?

The tax policy impact of the 2017 Tax Cuts and Jobs Act has ignited debates among economists and policymakers. Supporters argue that lower corporate tax rates encourage investment and growth, while critics highlight the revenue losses and question the modest wage increases. Recent analyses suggest that expired provisions for capital expensing might have been more effective than the tax rate cut in driving investment.

What lessons can be learned from the implementation of the 2017 Tax Cuts and Jobs Act?

The implementation of the 2017 Tax Cuts and Jobs Act provides valuable lessons about the relationship between corporate tax policy and economic behavior. Studies show that while corporate tax cuts do lead to increased investments, their effect on wages may not be as pronounced as anticipated. Future reforms may benefit from reinstating effective tax provisions that directly encourage business growth rather than solely focusing on rate cuts.

| Key Point | Details |

|---|---|

| Corporate Tax Cuts | Reducing the corporate tax rate from 35% to 21%, which was projected to reduce federal corporate tax revenue by $100-$150 billion per year. |

| Child Tax Credit | More generous Child Tax Credit provisions set to expire, impacting households significantly. |

| Impact on Investments | Corporate investments increased by 11% as a result of TCJA provisions enabling immediate write-offs for new capital investments. |

| Tax Revenue Effect | Corporate tax revenue fell by 40% initially but rebounded strongly starting in 2020. |

| Partisan Debate | The 2017 Tax Cuts and Jobs Act remains a contentious topic in political discussions, with varying views on corporate tax policies. |

Summary

The 2017 Tax Cuts and Jobs Act has redefined the landscape of corporate taxation in the United States. As key provisions near expiration, the ongoing discourse around this landmark legislation continues to influence the political arena, with divergent opinions on its effectiveness and future implications. With insights from notable economists like Gabriel Chodorow-Reich and ongoing debates regarding tax policy, the outcomes of the TCJA are both pivotal and complex, highlighting the need for continued analysis and potential reform.